The following is an excerpt from our quarterly newsletter distributed to clients.

Strong Quarter to End a Historic Year

Stocks and other risk assets experienced strong returns during the fourth quarter of 2020 as a relatively benign US presidential election outcome coupled with multiple COVID vaccine announcements encouraged investors to look towards better times ahead and in particular, a continued economic rebound in 2021.

The quarter saw a continuation of a trend that started mid-year. Stocks that benefit from an eventual economic recovery have been outperforming since June while stocks that benefited from the COVID “work from home” theme have started to meaningfully lag.

During the fourth quarter, Focus equity and credit strategies significantly outperformed their respective benchmarks. We will expand on the various strategies later in the letter.

2020 – a Brief Recap

2020 almost defies description, and we suspect that it will take years to fully grasp what occurred during the 12-month period. From an investment perspective, it was a year like no other. However, if we had to distill the year down, we would say 2020 was a story of two distinct investment phases.

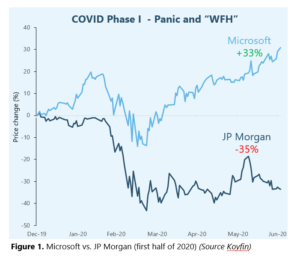

Phase I – Panic and “WFH”

The beginning of the first phase was characterized by market panic, uncertainty and indiscriminate selling. Yet after a historically quick and violent decline in March, markets recovered, largely as a result of the extraordinary support from governments and central banks. To the consternation of most value-conscious investors, the stock market recovery was not very broad. It was dominated by a group of companies that were well-positioned for a pandemic. The technology sector in particular, which allowed people to “work from home” and keep much of the economy functioning during the initial lockdown, was rewarded by investors. In our Quarterly Focus for the second quarter, we presented the chart below on the left (see Figure 1) to illustrate the massive divergence in returns between the technology sector and the traditional economy (using Microsoft and JP Morgan as examples).

Phase II – The Recovery

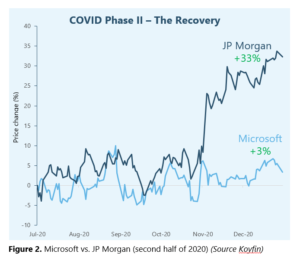

Interestingly, the publication of this chart coincided with the end of the first investment phase of 2020 and the start of the second – the recovery. Although broad market indexes such as the S&P500 and S&P/TSX seem to have continued their upward march almost uninterrupted, since late June the leadership under the surface of the market has shifted away from the “COVID winners” and towards stocks that stand to benefit from an eventual global recovery. To illustrate this point, we have updated the chart to show the second half of 2020 (see Figure 2). As can be seen, JP Morgan staged a recovery while Microsoft is lagging.

The second half of 2020 has therefore been much better to long-term value-conscious investors than the first half. Yet despite the strong moves in the second half of 2020, many stocks are still trading significantly below their levels of a year ago. This is particularly true for some traditional areas of the market favoured by value investors. These areas include energy, financials and real estate. As such, 2020 was a surprisingly tough year for value-conscious managers, many of which had a reputation for doing well in previous market downturns.

Consider Fairfax Financial, a former holding. Fairfax is led by Prem Watsa, who is often referred to as “Canada’s Warren Buffett”. Fairfax shares were down by 30% last year, a reflection of the difficult environment for many “deep value” investors (see Figure 3).

As we look forward into 2021, we suspect that we will see a continuation of the “Phase 2 – recovery” theme mentioned previously. Many companies that have been affected by COVID are still trading at the low end of their historical valuation range and their businesses will likely start showing improving trends in the coming quarters. We will describe a few portfolio holdings that share these characteristics in the upcoming Core Equity section.

By contrast, many companies that have benefitted from COVID may have “pulled forward” demand for their products, resulting in much more subdued growth figures expected over the next year at a time when their shares are valued near their historical highs. To wit, Microsoft may be an excellent company, but it may not make for a good stock for the foreseeable future.

In hindsight, the stock market moves in the first half of 2020 were largely a reflection of a rush to the safety of a relatively small group of very large stocks that weathered the COVID pandemic well. Since midyear, we have seen a broadening out of market leadership and a material rotation away from “Phase 1 – work from home” and towards “Phase 2 – recovery” stocks. Despite markets being at or near all-time highs, we believe there are plenty of attractive investment opportunities for patient investors who are willing to look beyond the current admittedly-challenging COVID second-wave situation.

Company Spotlights

Element Fleet Management

One of the top positions in Core Equity is Element Fleet, the largest commercial vehicle fleet management company in North America. We like Element’s business model for its significant barriers to entry, high recurring revenue and strong free cash flow generation. Since joining the company two years ago, CEO Jay Forbes, who owns a significant amount of stock, has done an admirable job returning Element to its dominant market position by re-capitalizing the balance sheet, exiting non-core business lines, cutting costs, improving customer satisfaction and overhauling the corporate culture. Rapid growth in “mega-fleets” (e.g. Amazon is a large customer) and continued conversion of self-managed fleets by governments and corporations facing balance sheet pressures support an attractive revenue growth outlook. Margin expansion, higher returns on capital and strong free cash flow will go toward reducing debt, buying back stock and growing the dividend. Element is a high-quality compounder-type company, and we believe this stock could double over the next 3-5 years.

Bausch Health Companies

A more opportunistic investment thesis would be Bausch Health Companies, a medical device and specialty pharma company. Bausch is a diversified mix of high-quality, valuable franchises (Bausch + Lomb eyecare) and other more mature businesses, which combined do not resonate with certain healthcare investors who are looking for “pure-plays”. We have long believed that the sum-of-the-parts valuation was well above the current share price, but this was largely a theoretical exercise until recently when the company announced that it will spin off its eye care business in order to realize shareholder value. Conservative assumptions imply a value 50% above the current share price.

Focus Private Investment Strategies

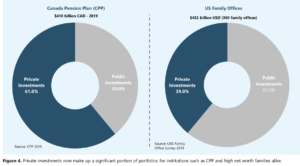

As communicated in a recent video sent to clients, during the quarter Focus successfully launched two new strategies to enable clients to gain access to private markets – i.e. investments that are not “public” and do not trade on a stock or bond market. The private investment world has grown to a point where it now rivals the public markets, and private investments now make up a significant portion of portfolios for institutions such as Canada Pension Plan and high net worth families alike (see Figure 4).

The advantages of private investments to a portfolio include:

- Enhanced returns

- Lower portfolio volatility

- Inflation protection

Closing Comments

2020 was a busy year for Focus. We believe we are coming out of the COVID downturn energized and with positive momentum. We have introduced several new strategies to help clients navigate what may be a tricky investment environment in the future and we are working with clients from a planning perspective to help them realize their wealth management objectives. At the same time, our core investment engine is benefitting from a resurgence in fundamental investing, and we expect that to continue.

Although we are excited about our stock holdings, it is important to point out that we are currently observing a fair amount of frothiness in some areas of asset markets due to speculative behavior. These areas include e-commerce and cloud computing stocks, Bitcoin and anything alternative energy and electric vehicle-related. On that last note, perhaps the single largest example of this phenomenon is Tesla. Although we won’t argue with any fans of the cars themselves, what has occurred to Tesla’s stock will likely be one for the history books. It has recently been added to the S&P500 as the sixth largest company, and the largest stock ever to enter the index. At a total company value of almost $700 billion, Tesla is worth more than the nine largest global auto companies combined, while producing a fraction of the number of cars (less than 1%). How this becomes relevant for investors is that index funds will be buying the stock after it has appreciated eight-fold from its March low and at an extremely high price and extended valuation. Index fund buyers beware.

Although perhaps the most egregious, Tesla is but one example of excess. However, we don’t want to leave the impression that we are overly negative. Speculative stock market episodes have come and gone in the past without derailing the entire market. For example, in the two years following the last major “new economy” bubble of 1999/2000, the NASDAQ index declined by almost 80% while the average stock actually appreciated.

In closing, the most-asked question of 2020 was: “How come markets are doing so well when the economy is doing so poorly?”

This was an understandable question given the strange combination of buoyant stock markets and global unemployment levels not seen since the Great Depression.

In hindsight, for a good part of the year, only certain parts of the market were doing well, which had an outsized effect on the market as a whole. More recently, those areas are now starting to lag while the rest of the market has seen a significant improvement.

As the global economy continues to recover from COVID, 2021 might see the opposite dynamic as 2020. Major stock market averages could tread water even as many undervalued stocks perform quite well. After 2020, anything is possible.