Our succinct perspective on key investment and wealth-related issues.

In the last 6 months, financial markets have been experiencing a shift, characterized by the following:

- The economic outlook for 2021 and beyond has improved

- Commodity and other input prices have firmed, while cyclical investments have outperformed

- The yield on the ever-important 10-year US Treasury Bond has more than doubled

It is no wonder that investors are starting to question the potential for these variables to impact returns across various asset classes. And some observers are beginning to believe that higher interest rates and inflation are becoming a foregone conclusion.

Betting on one outcome may not be the optimal approach

Admittedly, forecasting the long-term direction of inflation and interest rates has never been easy, and market experts have not been overly successful at predicting many of these macro variables. Recall oil at $150 per barrel before it fell to zero a decade later and think back to 18% mortgage rates nearly four decades ago before they recently touched 2%. While we at Focus are not inflation bulls, we are quite open to the possibility that the massive amount of fiscal stimulus required to keep economies afloat during the COVID pandemic combined with central banks’ willingness to continuously print money, could one day exert undesired consequences on the purchasing power of a dollar and on borrowing costs. Hence, we have given some thought to what this once “unthinkable” scenario of rising inflation and higher interest rates could do to various asset class returns if it continues, and we offer our perspective on how to generate portfolio returns without making a “one-way bet” on a specific outcome. The good news is that we think investors can prosper across numerous asset classes or at least mitigate much of the risk of being badly hurt if inflation and interest rates return to more normalized levels.

A healthy perspective on interest rates

Prior to sharing our thoughts on what to do from a portfolio perspective, we think it is healthy to review a graph of 10-year US Treasury rates to establish a longer-term perspective on where we stand today (see Figure 1). Clearly, falling rates have been a major contributing factor to returns across many asset classes during the past four decades. Notice the inverse relationship between interest rates and stock market returns. In fact, equity markets have advanced by more than double the rate at which earnings have grown in the past 40 years. In our view, there is no question that declining interest rates have impacted asset prices.

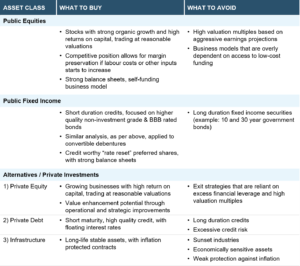

Simple strategies for generating returns without betting on a single outcome for rates

Markets are quick to judge

Although the above table is a rough guideline only and each security or investment opportunity needs to be analyzed individually, the overriding message is that the 40-year trend of investing across “long duration” assets with low discount rates and high multiples of earnings, may not produce attractive future returns now that interest rates are near a secular bottom. More concerning is that the favorable tailwinds from this strategy may be especially vulnerable if interest rates rise. Perhaps it has already started as richly valued stocks (characterized by high or no p/e multiples), resting on a foundation of ultra-low discount rates, have started to underperform the more attractively valued and less vulnerable parts of the stock market. It is likely no coincidence that since August, as 10-year Treasury yields have nearly doubled, the FAANG + Microsoft group of stocks have significantly underperformed the rest of the stock market.

With inflation and interest rates near secular lows and the increasing uncertainty around their future direction, we think it’s time to engage in new thinking about how to generate returns in what could prove to be a new era.